Despite stable income streams, over 60 million adult Americans have no access to or are denied access to traditional credit facilities. Credit and loan companies have a lot of red tape to filter out “high-risk borrowers,” who are often hard-working adults who have temporarily fallen into financial trouble or are working to improve their credit scores. Some companies sympathize with the plight of these affected demographics, recognize their business potential, and actively invest in providing credit access for these underserved individuals.

One of these companies is Opportunity Financial, or OppFi, which is publicly traded on the New York Stock Exchange under the ticker symbol OPFI. The company offers an alternative investment option to conventional banks and provides a technological edge that investors love.

So, let’s talk about the company—and why it might deserve a place in your portfolio.

What Is OppFI (OPFI)?

OppFi is an American specialty finance company that utilizes digital financial solutions to provide credit access to everyday Americans. The company uses AI-driven algorithms to match customers with the best credit options that fit their needs.

OppFi’s automation platform makes fully automated lending decisions for 73% of all applications in 2023, and these applications typically reach 250k a month. So, it’s fair to say that OppFi’s services are hitting its target market.

The question is, is the business flourishing?

Let’s look into its financials for the answer.

OPFI’s 2023 Annual Report

OppFi ended 2023 with excellent results. The report highlights a 12.4% YOY increase in total revenue, reaching $508.9 million. Basic and adjusted net income also grew by 1,082% and 771.2%, respectively—not an easy feat. Finally, adjusted EPS for FY’23 exceeded last year’s by 763%. 2023 also marked the company’s ninth year of consecutive net income.

“OppFi is confident it can continue its growth trajectory into 2024 and beyond. “We’re excited to begin 2024 and leverage our strong 2023,” said Todd Schwartz, OppFi’s Chief Executive Officer and Executive Chairman. “This year, we expect to continue focusing on profitable growth by maintaining prudent risk tolerances and scaling operating expenses efficiently.”

The company’s 2024 guidance reflects this modest optimism, though some analysts have called the outlook “soft.” Total revenue is expected to reach between $510 million and $530 million, representing a 4% increase on the high end. Meanwhile, adjusted EPS is anticipated to end between 53 and 57 cents, reflecting an 11.76% growth at the high end.

Analyst Recommendations

The company is not the only one bullish about its prospects. Analysts covering OppFi have given it a strong buy recommendation with a high target price of $6. Based on current prices, this represents an excellent 127.27% upside opportunity for interested investors.

Increasing Shareholder Value

“We ended 2023 with a strong balance sheet that provides us with optionality to create additional shareholder value,” Schwartz says in the 2023 report.

OppFi recently announced a special dividend of 12 cents per share, payable on May 1, 2024. Assuming 12 cents is its payout for the trailing twelve months, it would translate to a 4.56% yield.

Additionally, the company has initiated a 3-year $20 million share repurchase program to improve shareholder value further. OppFI certainly has enough cash flow to pay a consistent dividend. However, no solid dividend policies have been implemented as of the time of writing.

Still, the company’s willingness to give back to its shareholders when times are good, plus its improving financial performance, makes me think that OppFi presents a good value investment right now.

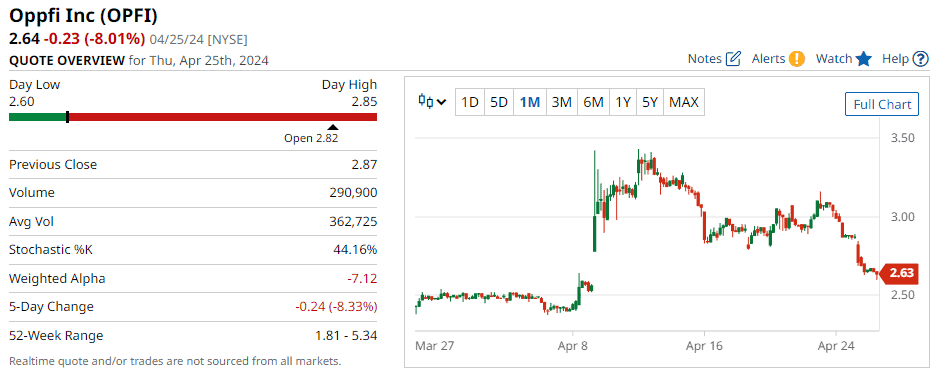

If that piqued your interest, you might want to know about OPFI’s price action to guide your investment decision.

What Does The Price Tell Us?

OPFI stock is valued at $2.65 per share, down 48.44% YTD. Prices are moving down, though they are nearing a solid support line at around the $2.43-$2.30 level. This presents a buying opportunity for investors banking on capital growth.

Using the Relative Strength Index (14-day) shows that prices have fallen below the 50 mark and are on their way to oversold territory. This tells us that other better buying opportunities might lie ahead when the stock settles over its established support line.

Final Thoughts

OppFi’s business model of providing credit services to underserved individuals is an attractive value proposition. The company is also showcasing significant growth, which can drive its prices up further.

Though the soft outlook has affected price performance, investors who believe in OppFi’s prospects, operational creed, and analyst recommendations might see this downturn as an opportunity to stock up on OPFI shares at a massive discount.

Related

Launch – Blog")

{kind=link}

Discussion about this post