Ahead of Donald Trump’s second term as US president, a rerun of his first trade war with China is firmly on the cards – and minerals key to the energy transition may end up in the crossfire.

The president-elect has threatened to raise tariffs on goods from China, as well as on other countries through which Chinese goods flow to the US.

While his overall stance towards China remains unclear, Trump has also pinpointed eliminating “dependence on China in all critical areas” as a priority.

Meanwhile, China has been developing a “versatile” policy toolkit to cope with rising trade tensions – including with the EU and Japan, as well as the US.

One notable recent example is China’s use of export controls, which it has placed on four minerals: germanium, gallium, graphite and antimony.

All of these minerals play important roles in low-carbon technologies, but also have other applications, including military uses.

Analysis by Carbon Brief and others shows that China’s initial export controls, introduced in summer 2023, did not have a sustained impact on critical-mineral supply chains.

However, an announcement in early December 2024 of stricter controls, specifically on exports to the US, has sparked debate over how impactful these might be.

In this article, Carbon Brief examines what US-China tensions over critical minerals could mean for the stability of their supply chains and for the transition to cleaner energy.

Which minerals are important to the clean-energy transition?

Minerals are crucial to the development of several low-carbon technologies.

Indium and gallium are used in the coatings for solar panels, copper and “rare earth” metals are used in the conductors and permanent magnets in wind turbines, and a plethora of minerals from lithium to manganese are used in various types of batteries.

China holds a significant presence in the supply chains for many minerals – particularly in terms of processing. As seen in the table below, more than half of global extraction of graphite, rare-earth elements (REEs) and vanadium, as well as the majority of processing of aluminium, cobalt, graphite, indium, lithium, REEs and silicon, occurs in China, according to a study by the Grantham Research Institute on Climate Change and the Environment.

A list of several minerals important for low-carbon technologies, plus the share that China holds in its reserves, extraction and processing industries. Source: Grantham Research Institute on Climate Change and the Environment.

However, not all of these materials are considered “critical minerals”, which is a political term used to describe those that play a role in strategically important sectors, with each country setting their own parameters for strategic importance.

The US lists 50 minerals as critical, while the EU has identified 34 critical minerals and an additional 16 “strategic raw materials”, while Japan has 35 minerals on its list.

Although China has not updated its official critical minerals list since 2016, a November 2023 post on the official WeChat account of the Ministry of State Security (MSS) revealed that it considers at least 31 minerals to be critical.

The post compares areas of overlap and divergence between the critical mineral listings of China (orange), and those in the EU (green) or the US (blue).

The diagram above shows a non-comprehensive list of minerals that the US (red), EU (grey) and China (blue) consider to be critical minerals, with minerals featured on two or more countries’ lists placed in the corresponding overlapping section. Source: Ministry of State Security, translated by Carbon Brief.

The minerals that are “on similar lists” for China and the EU and US are “where there’s more competition” when it comes to sourcing, John Johnson, special advisor and former CEO for commodities consulting firm CRU Group’s China office, tells Carbon Brief.

However, despite some countries’ efforts to diversify their imports of critical minerals away from China, analysis by the International Energy Agency (IEA) found that, based on announced projects, the status quo for supply of minerals such as lithium, nickel, cobalt and graphite was unlikely to change between now and 2030.

The IEA analysis noted that, in some areas, such as battery cell manufacturing, “announced capacity additions in Europe and the US should be sufficient to meet the 2030 domestic deployment needs” – although it added that, globally, demand for a number of critical minerals is likely to far exceed supply.

However, Tony Alderson, a senior analyst focused on graphite at price reporting agency Benchmark Minerals Intelligence, is sceptical, telling Carbon Brief that “it’s almost unheard of for a facility to be at 100% utilisation rates”. He adds that, for graphite, demand in the US and EU would likely outstrip supply well beyond 2030.

How has China’s ability to control its critical minerals evolved?

China has a well-documented history of using trade restrictions to achieve broader political aims.

The first trade war with the US between 2016 and 2020 saw China try to deescalate US tariffs on Chinese goods by imposing tariffs of its own, as well as non-tariff trade barriers.

The country has also used trade controls to affect non-trade-related political clashes.

Under the Biden administration, the US developed a “small yard, high fence” approach – meaning the US would “be selective in choosing technologies that need protecting, but be aggressive in safeguarding them”.

It placed a series of export controls on semiconductors and products used to make them, encouraging allies such as Japan and the Netherlands to do the same.

In response, China began limiting exports of some critical minerals, placing restrictions in August 2023 on exports of certain types of gallium and germanium, followed by similar restrictions on graphite from December 2023 and on antimony from September 2024.

With the exception of antimony, these restrictions were enacted in a clear response to US moves to curb Chinese imports for use in its semiconductor sector.

At the same time, China began enhancing its export control regime, which unified and rationalised an existing constellation of export control policies into a single framework.

This included development of an “unreliable entity list”, an export control law, legislation to counter foreign sanctions and regulation of items that are considered “dual-use”, meaning they can be used for military as well as civilian purposes.

“Historically, [China’s] export control regime has been extremely piecemeal,” Cory Combs, head of critical mineral and supply chain research at consultancy Trivium China, tells Carbon Brief.

He adds that one of the recent policy push’s major aims was to improve compliance by “making sure everything’s in one place and the rules are consistent – that you don’t have slightly different standards for different types of controls”.

These efforts paved the way to restrictions on critical minerals being intensified in early December 2024, when China sharpened restrictions on exporting graphite and banned exports of gallium, germanium and antimony to the US “in principle”.

A spokesperson from China’s commerce ministry stated this was in response to the US “weaponising” its own export controls by imposing broad restrictions on the Chinese chip-making industry.

How did the initial export bans affect critical mineral trade flows?

Analysis of China’s initial export controls on gallium, graphite and germanium shows that trade largely continued to flow, despite the new rules.

As shown in the graphs compiled by Carbon Brief below, Chinese exports of restricted types of gallium and germanium stopped for two months after the August restrictions came into effect. However, exports resumed from October 2023, albeit at slightly lower levels.

Not all types of the targeted critical minerals seemed to have been affected by the two-month suspension, with flows of non-controlled products, such as germanium oxides, seeing no significant change.

For graphite, exports of major products remained relatively stable, with the exception of a spike in exports ahead of the restrictions coming into place, likely due to stockpiling. Average exports in 2024 were higher than in 2022.

Both Combs and Johnson both note that, anecdotally, they had not heard of any cases of exporters being unable to acquire licences to export products.

Alderson tells Carbon Brief that exporters, nevertheless, found that the approvals were particularly quick for South Korea and Japan, while it took “longer for

-

A Beginner’s Guide to the Stock Market

Read more -

Biden Administration Sending Afghan Visa Applicants to Army Base in Virginia

$1.00 Add to cart -

Digital Marketing Strategy: An Integrated Approach to Online Marketing

Read more -

Forex Trading: The Basics Explained in Simple Terms

Read more -

Google AdSense + Chatbot Secret Exposed: How to Make $5000+ Monthly Even If You’ve Never Made a Dime Online

Read more -

")

How to Day Trade for a Living: A Beginner’s Guide to Trading Tools and Tactics, Money Management, Discipline and Trading Psychology (Stock Market Trading and Investing)

Read more -

How to Own Your Own Mind by Napoleon Hill

Read more -

How To Start a YouTube Channel for Fun & Profit 2022 Edition: The Ultimate Guide to Filming, Uploading & Making Money from Your Videos

Read more -

How To Win Friends and Influence People

Read more -

I Will Teach You to Be Rich, Second Edition: No Guilt. No Excuses. No BS. Just a 6-Week Program That Works

Read more -

")

MT4/MT5 & Trading View High Probability Forex Trading Method: TradingView Indicators now included in the download package (Forex, Forex Trading System, … Stocks, Currency Trading, Bitcoin Book 2)

Read more -

Rich Dad’s CASHFLOW Quadrant: Rich Dad’s Guide to Financial Freedom

Read more -

Secrets of the Millionaire Mind: Mastering the Inner Game of Wealth

Read more -

")

Social Media Marketing Workbook: How to Use Social Media for Business (2022 Online Marketing)

Read more -

The 10X Rule: The Only Difference Between Success and Failure

Read more -

The 4-Hour Workweek

Read more -

")

The Book on Rental Property Investing: How to Create Wealth with Intelligent Buy and Hold Real Estate Investing (BiggerPockets Rental Kit 2)

Read more -

The Complete Penny Stock Course: Learn How To Generate Profits Consistently By Trading Penny Stocks

Read more -

The Crypto Trader: How anyone can make money trading Bitcoin and other cryptocurrencies

Read more -

The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns

Read more -

The Magic of Thinking Big

Read more -

The Power of Habit: Why We Do What We Do in Life and Business

Read more -

The Psychology of Money: Timeless lessons on wealth, greed, and happiness

Read more -

The Richest Man In Babylon

Read more -

The Richest Man in Babylon

Read more -

The Science of Getting Rich

Read more -

The Science of Getting Rich

Read more -

The Strangest Secret

Read more -

The Wealthy Gardener: Lessons on Prosperity Between Father and Son

Read more -

Think and Grow Rich

Read more -

Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude

Read more

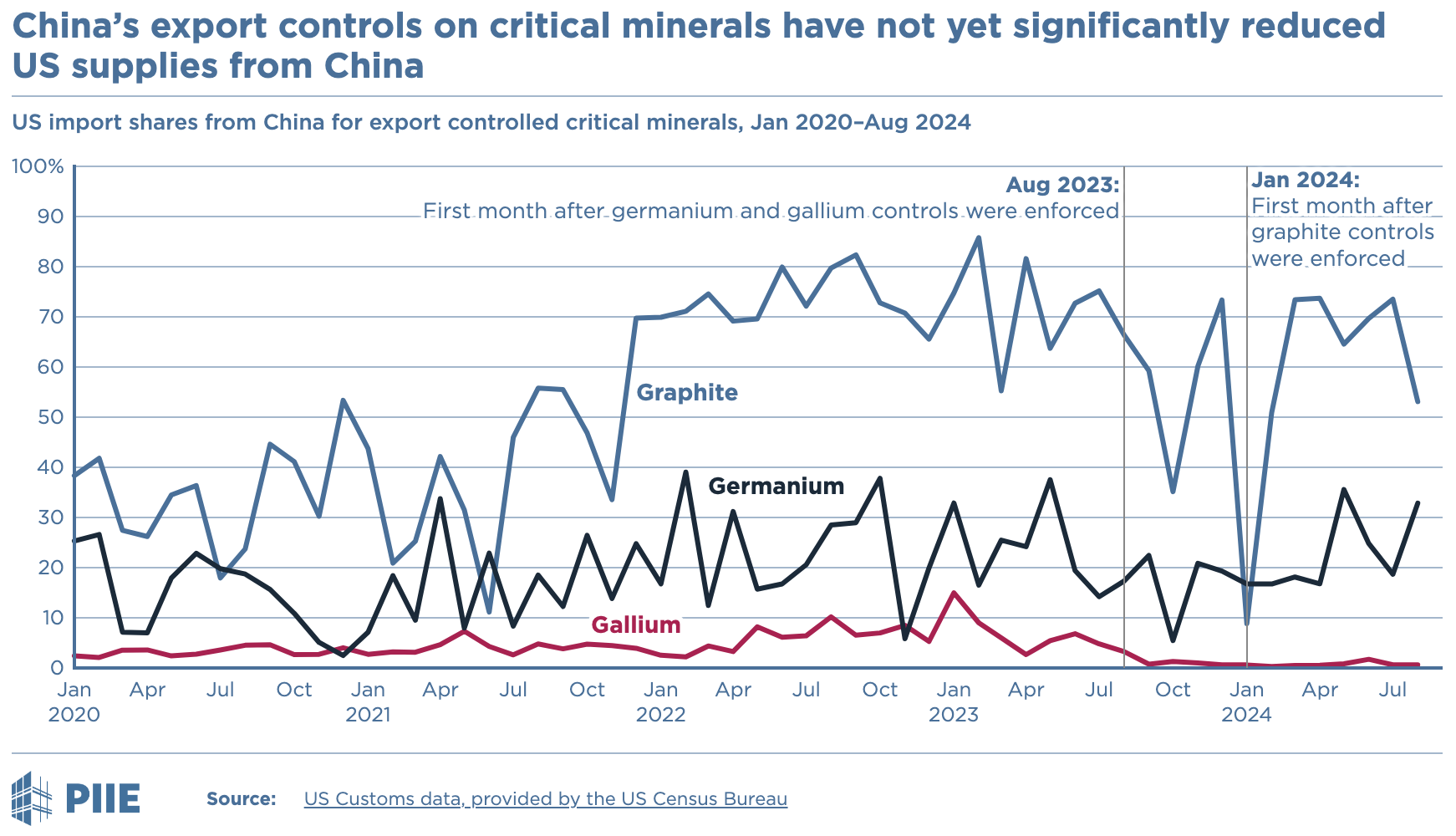

Analysis by the US-based Peterson Institute for International Economics (PIIE) similarly found that, for the US in particular, the export controls on gallium, germanium and graphite “haven’t radically altered the US-China trading relationship around these minerals and related products”, as shown in the graph below.

For graphite (the blue line in the chart), US imports from February to August 2024 were “only a hair lower than in the seven months preceding the announcement of export controls”, it found.

For germanium (black), in 10 months following the enactment of controls, exports were “down only one percentage point from the ten months preceding the ban”, it added. For gallium (red), while exports have fallen to zero, “the chart makes very clear [that] the US was never particularly reliant on China for sourcing in the first place”.

The PIIE analysis concluded in August 2024, ahead of the restrictions on antimony and US-specific controls.

This outcome was likely by design, due to the calculated nature of China’s export controls.

The goal of the initial export controls was to improve China’s visibility of how the minerals it processed were being used, Combs tells Carbon Brief, which is why the initial controls required exporters to apply for licences, rather than implementing a blanket ban on exports.

Alderson says that the new licences required companies to share more information about themselves, their products and their end users.

As such, cutting off supplies to other countries immediately was not the aim of the original announcements.

The initial controls on critical minerals broadly follow similar patterns to China’s previous non-tariff trade measures. With the exception of antimony, the critical mineral controls were imposed in response to perceived attempts to “undermine China’s national sovereignty, security, and development interests”, rather than being the first salvo of a trade dispute.

This is because, according to a Royal United Services Institute (RUSI) report, China is aware that outright export bans would accelerate other nations’ efforts to derisk and diversify supply chains, weakening its long-term position.

The RUSI report added that export controls must be examined to determine whether the move is meant to be a political signal or a more serious attempt at “economic coercion”.

Stringent export controls incur a domestic cost in China, impacting both industrial activity and broader economic growth. As such, export controls are likely to be calibrated to capture headlines without incurring as severe an economic impact as they imply, RUSI said.

A government official involved in the design of the gallium and germanium controls said they were meant to be a “deterrent”, the Financial Times reported, quoting the official saying: “We had many options…This was not our most extreme move.”

An example of China “going for the throat” with export controls, Combs tells Carbon Brief before the US-specific controls were announced, would be placing controls on copper.

He explains this is because – although Chinese copper is a vital resource in global manufacturing, particularly in clean-energy technologies – the majority of copper smelted in China is consumed domestically. As a result, an export control on copper “would be a perfect case of hurting others without hurting itself too much”.

“Instead”, he says, the initial moves seemed to be saying “don’t test us”.

Do the US-specific controls represent a significant change in China’s strategy?

The measures announced in early December 2024 are a pointed escalation of China’s use of critical mineral export controls.

Under the new rules, gallium, germanium and antimony will “in principle” no longer be permitted to be shipped to the US and tighter controls will be placed on sales of graphite.

In an analysis, Combs and Trivium China co-founder Andrew Polk wrote that the restrictions are a signal that China is “ready to counter US moves much more aggressively”.

This was echoed by China’s former central bank governor Yi Gang, who the South China Morning Post quoted saying: “We all understand that, from an economics perspective, [retaliatory actions are] never a good choice…but there’s not much policymakers can do about that [in the face of domestic pressure].”

More time will be needed to see “how strict” implementation will be, Alderson says, adding that for graphite, it is not yet clear which products will be affected – the stricter controls could be limited to “the 99.999% [purity] which goes into military end-use materials”, rather than the lower-grade graphite used in electric vehicle batteries.

Trivium China’s assessment noted that the announcement suggested China would “close” loopholes that allowed for “export leakage”, adding that it is not clear “how far Beijing might go to investigate or punish third countries suspected of prohibited re-exports”.

Gerard di Pippo, senior geoeconomic analyst for Bloomberg Economics, was sceptical about the significance of the threat, writing that “China lacks the legal reach, export-control surveillance capabilities and alliance network” needed to enforce third-country compliance.

Other analysts told MIT Technology Review that, “for the most part, the bans won’t have major economic impacts”, due to existing US efforts to diversify its supply chains

Nevertheless, Alderson says, the current uncertainty underscores the fact that “localisation is critical” for those that rely on critical minerals.

Could future US-China tensions exacerbate critical mineral controls?

China’s motive for the most recent controls is unclear, Combs and Polk wrote. It could be to protest against the US move to restrict exports of particular chips and chip-making tools as well as the addition of 140 Chinese companies to a trade blacklist, they said, or to “warn the incoming Trump administration” against raising tensions.

It is broadly expected that US-China trade tensions will escalate after Donald Trump begins his second term as US president.

US concerns around the “threat” that China poses to its industrial capabilities have been notably bipartisan. However, where Biden’s approach was characterised by relatively nuanced policies, the second Trump administration – much like the first – could prioritise the use of broad tariffs to shrink the US’ trade deficit with China.

Combs tells Carbon Brief that Beijing’s goal is to “change US behaviour”, so it would “use terms that Trump understands”, such as broad trade tariffs, in trade disputes with the US, rather than the more nuanced controls it has used in response to the Biden administration. He explains:

“Most of the [trade volume and value of these] minerals are way too small to affect the trade balance…so purchases of beef, soy and similar items would make more sense as a retaliation mechanism [for China to use].”

It remains to be seen, he says, how much emphasis Trumps’ advisors, particularly new commerce secretary Howard Lutnick, will place on critical minerals. The issue could appear on the radar should Beijing use additional controls to pressure particular US companies to lobby the US government, he adds.

Johnson notes that China has reasons to avoid escalating the issue of critical mineral exports further, such as its dependency on the US for exports of a number of minerals, such as high purity quartz, iron ore and potash.

In addition, he says, the minerals that countries consider critical “change over time”, as new technologies create demand for new minerals and render other minerals obsolete.

Progress in developing recycling processes could also relieve pressure on supply chains. Scrap is already a small source for supply of gallium and germanium, while germanium can also be recovered from existing products.

According to the IEA, successful scaling-up of recycling could “lower the need for new mining activity by 25‑40% by 2050”, under a scenario that assumes governments will meet all of their climate goals on time and in full.

Meanwhile, other regions seem to be treading cautiously. The Washington Post notes that pushback from the Japanese and Dutch governments led to a “delay” in the launch of the most recent US semiconductor export controls, which were watered down to “accommodate” their concerns.

Combs tells Carbon Brief that he does not see any flashpoints significant enough to trigger export controls on critical minerals to the EU.

“[Restricting China’s ability to buy from] ASML was the single most impactful [move against China by the EU],” he says, adding that there are few, if any, remaining political disputes where Europe would willingly trigger “significant retaliation” from China.

Sharelines from this story

{kind=link}

Discussion about this post