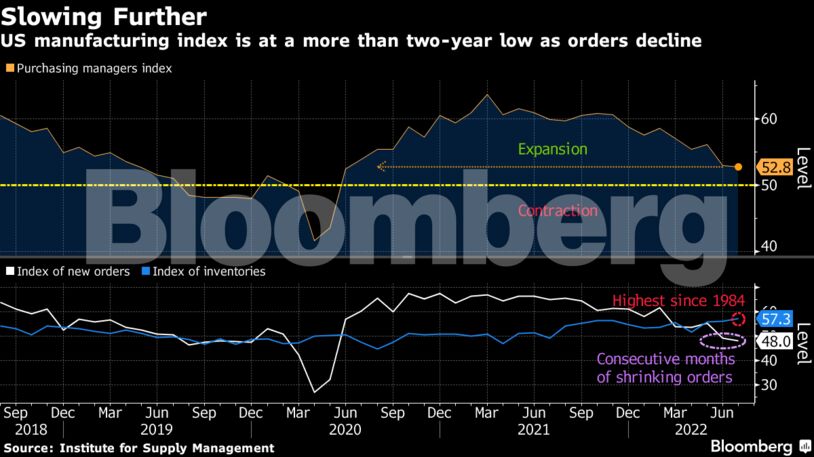

The group’s measure of production also fell to a more than two-year low, and its gauge of new orders remained in contraction territory for a second month. The figures highlight softer demand for merchandise as the economy struggles for momentum.

“Panelists are now expressing concern about a softening in the economy, as new order rates contracted for the second month amid developing anxiety about excess inventory in the supply chain,” said Timothy Fiore, chair of ISM’s Manufacturing Business Survey Committee.

The ISM factory inventories index rose to 57.3, the highest since 1984 and suggesting stockpiles are mounting at more manufacturers. While many producers have been adding to inventories in the event of further supply-chain disruptions, the increase may also suggest some of the build is unintended.

Separate data from S&P Global this morning showed a build-up in finished goods inventories for the first time since October 2020. That group’s final July overall factory purchasing managers index slipped to 52.2, a two-year low.

Past Year

The ISM overall index is down almost 11 points from its multi-decade peak in March of last year, when producers were scrambling to meet pent-up demand as the economy emerged from pandemic lockdowns. Spending on merchandise has since slowed as consumption patterns started shifting from goods to services.

Eleven manufacturing industries reported growth in July, led by apparel, minerals and petroleum and coal products. Seven industries reported a contraction, led by wood products, furniture and paper.

The ISM and S&P Global manufacturing data are consistent with a general slowdown in other parts of the world. European factory activity slumped last month and manufacturing output in Asia continued to weaken.

Purchasing managers’ indexes for the euro area’s four-largest members all indicated contraction, with shrinking confirmed for the region as a whole after an initial estimate on July 22. In Asia, it was China, South Korea and Taiwan that took the biggest hit.

Read more: World Factory Outlook Darkens With Weakening From Europe to Asia

The July measure of prices paid for materials used in the production process — extremely elevated over much of the last year and a half amid supply and demand imbalances — plunged 18.5 points to the lowest level in almost two years.

That marked the largest drop since 2010 and reflected declines in crude oil and metals prices. Almost 22% of respondents reported paying lower prices in July, up from 8.3% a month earlier, the report showed.

Select ISM Industry Comments

“Inflation is slowing down business. Overstock of raw materials due to prior supply chain issues and slowing orders.” – Chemical Products

“Chip shortages remain; however, the Covid-19 lockdowns in China are presenting even worse supply issues.” – Transportation Equipment

“Growing inflation is pushing a stronger narrative around pending recession concerns. Many customers appear to be pulling back on orders in an effort to reduce inventories.” – Food & Beverages

“New order entry has slowed down slightly; however, logistical issues have yet to improve. Long lead times for materials and labor shortages are still a major problem.” – Machinery

“Our markets are still holding up; however, I believe a slowdown is coming. We are cautious about going out too far with orders. Also, I believe the general market is in the beginnings of a recession.” – Fabricated Metals

“Current order books are full, but there have been signs of a slowdown beginning in the fourth quarter.” – Plastics & Rubber

Supplier delivery times lengthened, the purchasing managers data showed, yet at the slowest pace since before the pandemic. That, combined with declining orders, likely enabled firms to make progress on unfilled orders. The ISM’s measure of backlogs fell to the lowest since June 2020.

")

{kind=link}

Discussion about this post