[ad_1]

News headlines tell of Canadians pushed to the brink by rising mortgage costs. Some have been forced to sell their homes, and others don’t know where to turn, as their mortgages now cost thousands of dollars more each month than they did just two years ago.

Yet Canadians’ spending has not dropped as significantly as the Bank expected when it started raising rates. And the Canadian housing market remains stable enough, considering today’s high mortgage rates. How did we get here?

How average mortgage payments have changed since rate hikes began

During the first quarter of 2023, the average monthly payment on new mortgages in Canada was $1,984, up 40% from $1,415 in 2019, according to the Canada Mortgage and Housing Corporation (CMHC). And the average monthly payment on existing mortgages during the same period of 2023 was $1,551, up 20% from $1,277 in 2019.

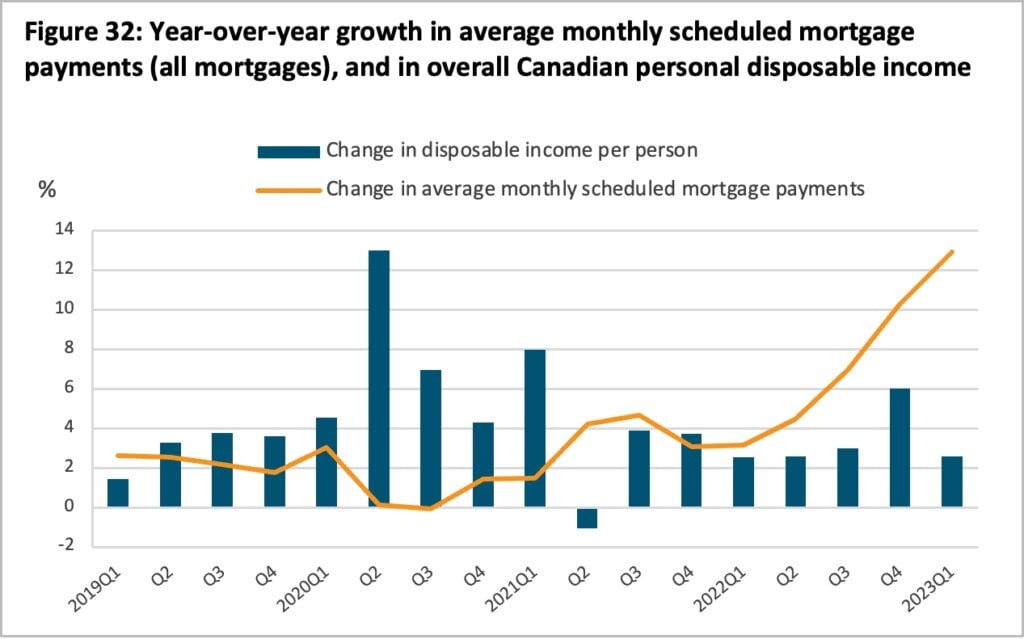

The rate at which mortgage payments are growing has accelerated and is now the highest it’s been in at least five years. Whereas monthly mortgage payments have often grown at an annual rate of 1% to 5% since 2019, the annual rate grew to nearly 13% during the first quarter of 2023.

How mortgage payments have changed across Canada

A look at the typical mortgage payment in Canadian cities reveals the biggest jumps occurred since early 2022, when the BoC began raising interest rates. The table below shows the average mortgage payment for large, medium and small census metropolitan areas (CMAs) for the first quarter of 2021, 2022 and 2023. The calculations come from CMHC and are based on Equifax data.

In many instances, average monthly mortgage payments grew only marginally between the first quarters of 2021 and 2022. Canada-wide, for example, the difference is $43 per month—similar to the increases seen in large, medium and small CMAs. But the situation changed drastically between the first quarters of 2022 and 2023, as average monthly payments climbed $179 across Canada and by more than $200 in large CMAs.

Why are some Canadians struggling more than others?

The numbers above are averages that include both fixed and variable mortgage payments. They’re helpful in understanding how typical mortgage payments have changed, but they do little to corroborate the tales of home owners whose monthly costs have doubled since rate hikes began. For that, we have to take a closer look at the difference between fixed and variable mortgage rates and do some calculations using a mortgage payment calculator.

According to CMHC data, the average new mortgage loan was $319,140 in the first quarter of 2021. We’ll use that number as a benchmark to calculate how rising interest rates have impacted fixed- and variable-rate mortgage borrowers differently.

The table below is an example based on average historical interest rates from Ratehub.ca and the mortgage renewal calculator on MoneySense. (Ratehub.ca and MoneySense are both owned by Ratehub Inc.) The calculations assume a $319,140 mortgage, obtained in March 2021 and amortized over 25 years, a term of five years and a down payment of 20%.

[ad_2]

Source link