Oil and fuel industries simply loved a bumper revenue 12 months, with shareholders seeing document payouts. In its wake, Europe’s Shell and BP each walked again on their formidable low-carbon transition plans, with corporations throughout the sector rising their investing in new manufacturing.

That’s not excellent news for local weather change, largely pushed by burning fossil fuels. One fear is these investments imply the business and its political allies will combat tooth and nail for them to keep away from “stranded belongings” losses, locking in increased manufacturing of local weather altering fuels for years and even a long time to come back.

Not solely the businesses, but additionally their shareholders may flip, as vested pursuits, right into a broad coalition towards inexperienced power. No less than within the U.S. and the U.Okay., most pensions are invested in capital markets, the place inside inventory markets oil and fuel corporations stay among the many most dependable turbines of dividends and share buybacks. All of this might deter governments from implementing all-too-ambitious local weather mitigation insurance policies for worry of inflicting monetary losses to a broad swath of their very own voters.

However based mostly on a latest evaluation, we argue that high-income governments needn’t fear about triggering these monetary losses. That’s as a result of most hits from stranded fossil gas belongings—decrease manufacturing volumes or gross sales at decrease costs than traders anticipated—would fall totally on the rich members of those nations. That ain’t most voters.

The reason is comparatively easy: these nations all have vital inequality in who owns corporations. Which means the rich usually personal the overwhelming majority of all shares and bonds, and there’s no proof that differs considerably within the oil and fuel sector.

Governments ought to certainly fear about potential results on the customers of fossil fuels, amongst automobile house owners for instance, brought on by carbon costs and different local weather insurance policies that impose penalties on consumption, and there have been necessary proposals for measures to cut back the adverse results of fossil gas phaseout on probably the most weak folks in society, akin to “carbon dividends” and improved public transport. Governments also needs to fear about workers within the power and different sectors and guarantee a simply transition for fossil gas communities. Nevertheless, for monetary investments, the underside 50 p.c and even 90 p.c of wealth house owners might be compensated at little or no value in comparison with these different measures.

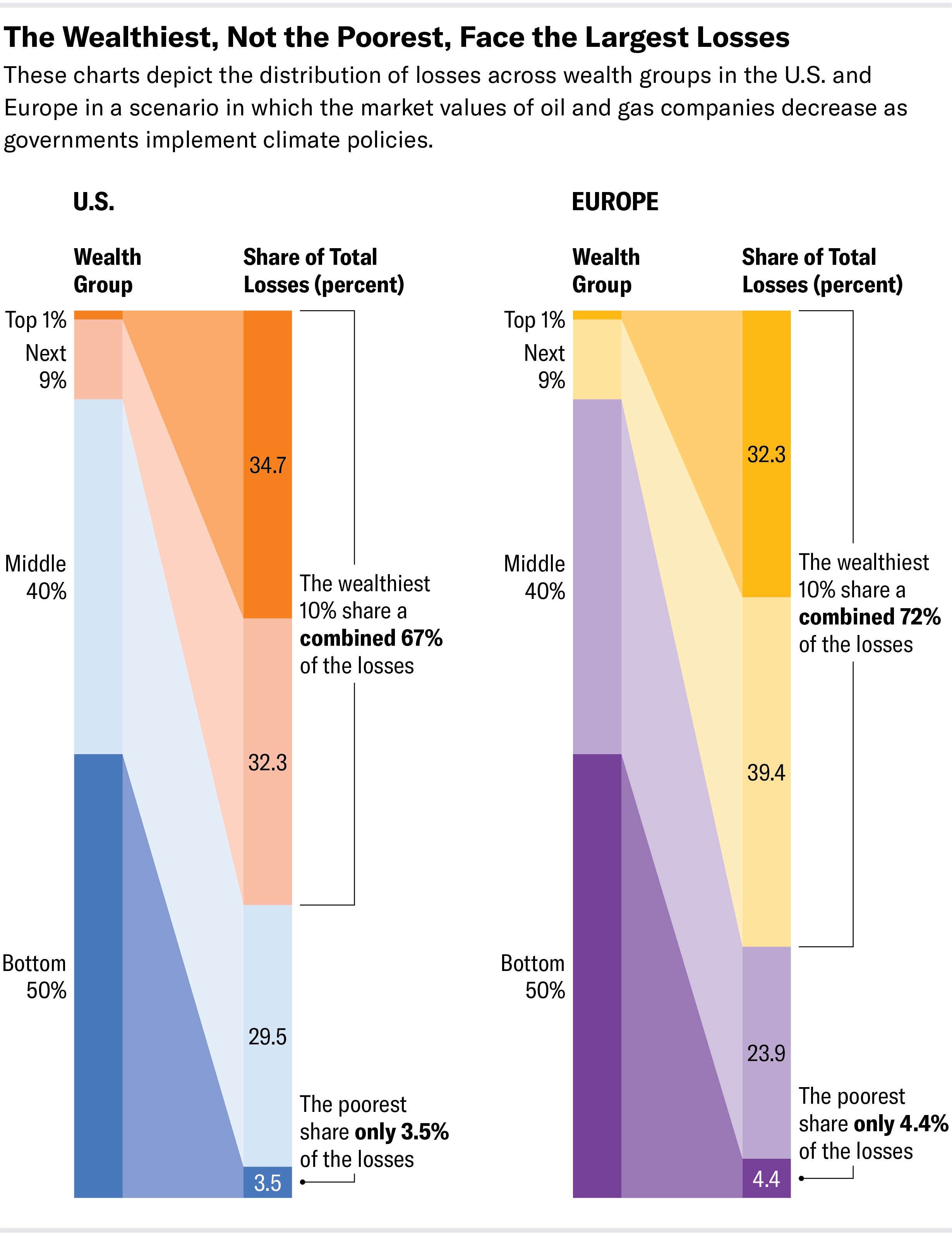

Now we have beforehand calculated that in a situation the place oil and fuel corporations are initially valued based mostly on an expectation of participation in a rising oil and fuel market, however governments world wide implement local weather insurance policies limiting world warming to 2 levels Celsius above preindustrial averages, this might result in wealth losses of almost $550 billion for U.S. and European shareholders as corporations’ market values are readjusted to those decrease expectations. Nevertheless, as soon as we analyze the place these shareholders are prone to sit within the wealth distribution, it seems that solely 3.5 p.c within the U.S. and 4.4 p.c in Europe of the losses hurt the portfolios of the underside 50 p.c of them (see chart). Merely put, those that personal most shares, additionally personal a lot of the oil and fuel sector shares that get devalued.

As a result of the highest 1 p.c and prime 10 p.c are so rich nonetheless (each U.S. American grownup within the prime 1 p.c owns greater than $13 million in internet wealth on common) these losses, unfold throughout people, hardly present of their portfolio. We estimate that losses quantity to lower than half a p.c of the web wealth of wealthiest 1 p.c or 10 p.c of People, for example. Furthermore, as fossil fuels decline, new funding alternatives emerge within the rising markets for low-carbon options that permit for portfolio hedging. Even losses for the least rich 50 p.c and 90 p.c are usually not excessive as a proportion of their wealth. The priority may come up from the truth that they’ve so little wealth within the first place. Compensating the underside 50 p.c would value simply $12 billion within the U.S. and $9 billion in Europe in a $550 billion loss situation. This might be paid off with only one sixth of the annual income from a notional $13 per ton of carbon dioxide emissions value within the U.S., which is far decrease than present consensus estimates of the social value of carbon. In Europe, it is also paid off with round 20 p.c of the income from the European Emissions Buying and selling System (ETS) in 2022.

One may argue that the wealthy are rather more refined traders and can get out of their investments earlier than the shares lose their worth, saddling the poor with rather more of the losses. That is certainly a priority, but our robustness calculations recommend that even when the poor had been more likely to personal oil and fuel shares, compensation prices would stay restricted.

There are lots of obstacles to shifting away from fossil fuels, from costs for shoppers and corporations to employment and which means in communities the place fossil gas manufacturing is concentrated. Governments should tackle all of them rigorously. Nevertheless, losses for monetary traders don’t rank amongst them, and even when they had been, we present that compensation for any socially related losses can be low cost certainly.

Warnings about pension losses and pushback towards measures that may trigger asset stranding seem largely made within the curiosity of the very rich, whose capability to soak up losses is arguably a lot increased than everybody else’s. Losses from unmitigated local weather change, alternatively, will probably hit the poor and weak a lot tougher.

That is an opinion and evaluation article, and the views expressed by the creator or authors are usually not essentially these of Scientific American.